In an earlier blog, we discussed How Credit Scores Can Result in an Insurance Discount. What follows is a more in-depth analysis of how the process works. When you understand how policies are priced, you gain knowledge that will help you control your own insurance destiny. From here, you can take steps to reap rewards in the form of greater discounts. Let’s review.

Everything You Need to Know About How Your Credit Score Impacts What You Pay for Insurance

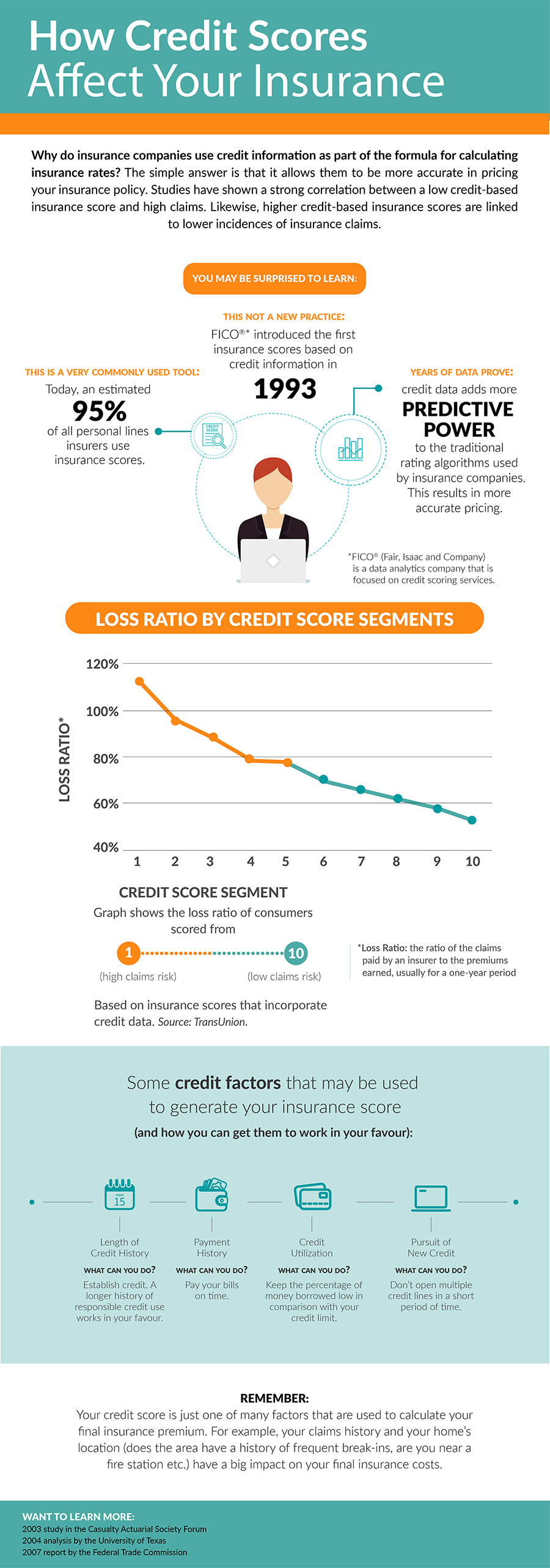

Background

The use of credit scoring isn’t new. The concept began nearly three decades ago (1993) when FICO® (Fair, Isaac and Company) first began applying insurance scores to measure risk and ultimately calculate insurance pricing. For the uninitiated, FICO® is a data analytics company that is focused on credit scoring services. FICO® Insurance Scores are credit-based insurance scores. You’ll find these scores under different names, such as the Canadian Property Loss Score (CPLS™) at Equifax Canada or the FICO® Insurance Risk Score at TransUnion. Is using your credit score to calculate insurance risk accurate? Data certainly says so.

The Insurance Information Institute reports on numerous studies which have verified a strong relationship between credit scores and claims experience. Insurance scores significantly improve risk prediction when combined with traditional risk assessment variables, which in turn improves pricing accuracy. The same report finds that the Federal Trade Commission (FTC) also concluded that insurance scores allow for more accurate underwriting and risk pricing. To date, over 95% of Property and Casualty (P&C) insurance companies (home, tenant, auto etc.) and personal lines insurers alike use credit scores to determine policy premiums.

It Most Likely Works In Your Favor

It’s important to understand that this system of policy calculation is steeped in fairness, with the goal of distributing premiums fairly based on the customer’s corresponding risk. Reports state that approximately 50 percent of policyholders end up paying lower premiums because of good credit. What about the other 50%? Studies find that credit scoring ended up being a neutral factor for about 25% of the remaining policyholders. Of course, that means the approximately 25% of policyholders may pay higher premiums. However with this system, those higher premiums are more accurately distributed to those parties that pose the highest claim risk.

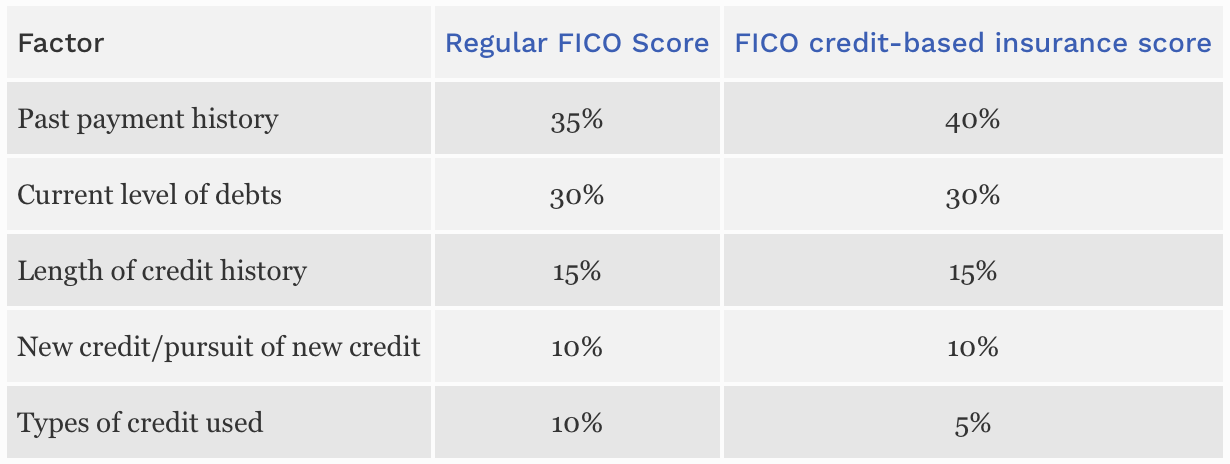

Difference Between Your Credit Score and Credit-Based Insurance Score

How you manage your finances impacts your credit score and your credit-based insurance score in similar ways. However, there are a few small differences. This is how FICO delivers weight to each:

Source: FORBES March 2020

How to Improve Your Credit-Based Insurance Score

Based on the weighting scale above, you quickly see where you can make adjustments to improve your credit score and ultimately your credit-based insurance score.

-

- Past Payment History – Pay all bills and account liabilities early or on time.

-

- Current Debt Level – Keep the percentage of money borrowed low in comparison with your credit limit.

-

- Length of Credit History – Establish/re-establish credit. A longer history of a responsible credit use works in your favour.

-

- Pursuit of New Credit – Don’t open multiple lines of credit over a short period of time.

-

- Types of Credit Used – Build a diverse credit portfolio. FICO (and Equifax) like to see responsible use of various types of credit, such as installment loans (auto loans, student loans), mortgage loans, and credit cards (bank, retail).

Don’t Forget Traditional Insurance Discount Qualifiers

Your credit score is just one of many factors that are used to calculate your final insurance premium. Traditional criteria applies all the same, which includes (but is not exclusive to) your claims history and your property’s location as it pertains to risk (i.e. high crime area, flood and wildfire zones etc.).

If you have any additional questions about how Park Insurance calculates your insurance premiums and discounts, please contact Park Insurance to schedule a consultation today.

Enjoy our infographic below, and please share it with your friends and colleagues: