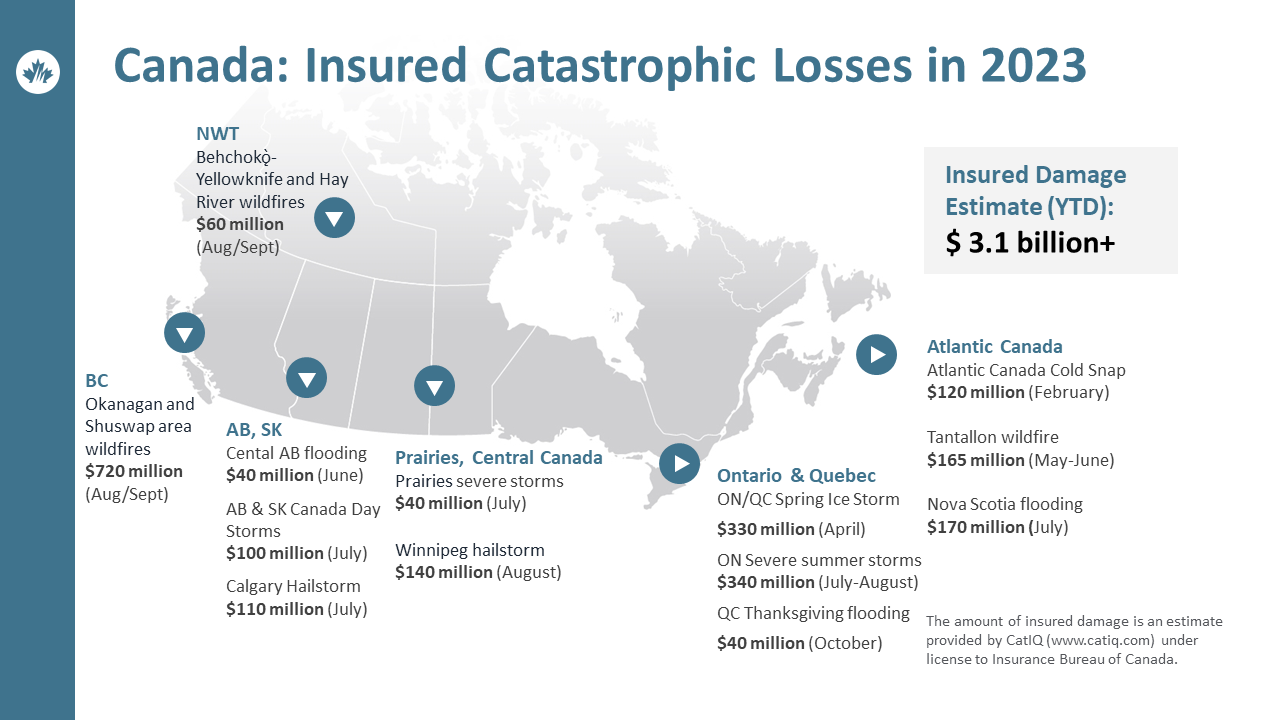

For the second consecutive year, Canada has surpassed the $3 billion mark in insured damage caused by natural catastrophes and severe weather events. In 2023, severe weather events led to a national total of over $3.1 billion in insured damage, as reported by Catastrophe Indices and Quantification Inc. (CatIQ).

While a significant proportion of households fell victim to the effects of extreme weather, businesses also faced the brunt of its wrath. From flood to fire, business interruptions went through the roof, which not only disrupted commercial enterprises themselves, but the people who depended upon them for employment along with access to products and services. Is there anything that you as a business owner can do to protect yourself this year? Or are you powerless against a force as enigmatic as climate change? Let’s find out.

What BC Businesses Need to Know About Protecting Themselves Against Interruption Caused by Climate Change

You need to batten down the hatches for your brick and mortar, taking preventative measures that will reduce the risk of damage and loss due to weather events that are common to your service area. This is especially important as construction costs for rebuilding in BC are skyrocketing. Throughout the years, Park Insurance has assembled guides to help BC businesses accomplish exactly that. Whether you’re established in communities that are vulnerable to summertime wildfires, late winter flooding from snowmelt, both, or everything beyond and between, we’ve got you covered. Please reference the following guides as they apply to your location(s):

- Wildfire Protection Plan for Your BC Business

- How to Protect Your Shop or Office Space from an Approaching Forest Fire

- Flood Preparedness Plan for Your BC Business

- How to Protect Your Shop or Office Space from Snowmelt Flooding

- How to Protect Your Business from Extreme Winter Weather

Don’t Forget Disruption of Online Operations Too

Extreme weather may be “best known” for disrupting access to (and functions within) shops, stores, and commercial office spaces, but it can also shut down online operations. With digital transformation leading the way to company success in 2024 and beyond, such interruptions can be severely damaging. For this reason you may want to consider reducing reliance on on-premises servers and migrating all digital assets to the IT cloud.

While most business leverage the cloud for data storage, ensure that you do the same for productivity as well. Secure cloud-based software-as-a-service (SaaS) solutions such as MS 365 or Google Workspace so that workloads are maintained in a cloud environment. This way, if a lightening storm or wildfire knocks out your power grid, all work-in-progress will be saved in real-time and will be accessible from any remote location. Ongoing projects along with consumer and stakeholder communications can be picked-up right where they left off, without significant interruption.

But, remember that online operations come with their own risks, so stay vigilant about cyber security and ensure you have adequate cyber insurance protection.

Does Business Interruption Insurance Cover Weather?

The best way to protect against business interruption? Business interruption insurance of course! While commercial property insurance covers the cost of repairing your building and/or equipment damage, business interruption insurance can help you recover and maintain revenue in the meantime. It’s the key to getting your business up and running again in the most timely manner possible. However, you may be wondering if such a policy covers disruptions that may occur from extreme weather events. Good question. While dependent upon your specific policy, you may absolutely be covered for cessation of operations that prevent your business from generating revenue during and after a weather event. But, it is important to understand that business interruption coverage is triggered by loss or damage to your physical property by an insured peril. It does not apply if customers are not shopping due to a severe weather event or other issues in the area. For example, there would not be coverage for business interruption if business is slow because a fire in a neighboring town prevented traffic from getting through.

A broker at Park Insurance can help you understand what is, and is not, covered by business interruption insurance and help you determine if this coverage is right for you. In some cases, you will also want to supplement your business interruption insurance coverage with riders such as equipment breakdown insurance. Simply put, while business interruption insurance does protect you against climate change in many ways, you may need to consider add-ons for your policy, for added peace of mind.

Park Insurance is ready to help you ensure that your existing commercial / business insurance and business interruption policies are enough to protect you, staff, and customers/clients against all of the variables tied to climate change. Schedule a comprehensive review of your commercial policies today. Call 1.800.663.3739 right away.