BC premier, John Horgan, recently remarked that price for lumber is ‘just off the charts’! Some sources state that lumber supplies for the construction of new single-family homes have tripled over the past year!

Reconstruction Costs Are Skyrocketing! What You Need to Know About Your Insurance Coverage.

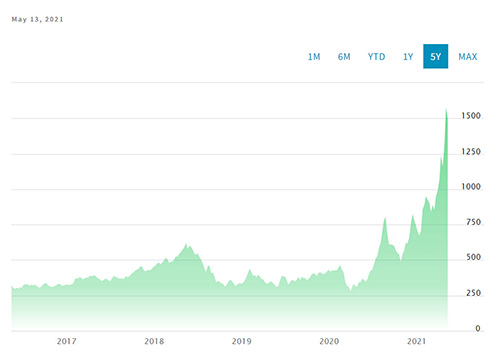

The following Nasdaq chart, depicting lumber prices per thousand board foot, clearly illustrates the unprecedented spike.

“The current lumber market is a confluence of limited supply – both long term and short term – and exceptional demand.” Reuters

Many homeowners who found themselves stuck at home in 2020 decided it was time to renovate, creating a surge in demand, not just for lumber, but for other building materials as well.

However, this spike in construction costs may mean more than just delaying a renovation project. What you may not have considered is that soaring lumber prices affect the amount it would cost to rebuild your home in the event of a claim.

The amount of insurance that you purchase should based on the amount it would cost to rebuild your home in the event of a total loss. So, understandably as material costs soar, the cost to rebuild your home also increases significantly. How does this affect your current insurance policy? The answer is that it depends on the type of policy that you purchased. (Learn more about the difference between your home’s market value, assessed value and replacement value.)

Let’s take a look at a few different scenarios:

Actual Cash Value Policy

Actual Cash Value pays to repair damages or replace your building or your possessions—minus a deduction for depreciation. With building costs skyrocketing, it is essential that you call your broker to review your property’s valuation, today!

Replacement Cost Policy

Replacement Cost policies pay to repair or rebuild your home at the actual cost to replace it. However, it is important to note that you are only covered up the amount of insurance you purchased. For example, if your policy limit is $400,000, but at today’s construction prices it costs $800,000 to rebuild your home, the maximum payout would be $400,000. The remaining $400,000 would need to come out of your pocket!

Under-insuring your home does not only affect you in the event of a total loss. If your home is partially damaged, and you are only insured for half the current replacement value, the insurance company will only pay half of the costs to make repairs and you will have to pay the difference yourself. This is known as a co-insurance clause. With building costs skyrocketing it is essential that you call your broker to see if you need to increase your home’s valuation, today!

Enhanced Replacement Cost Policy

An Enhanced Replacement Cost policy typically pays 10% to 15% above your limit, just in case it costs a bit more to replace or rebuild your home after a loss. Typically, this buffer would be enough to offset any increases in construction costs. However, with the unprecedented spike we are currently seeing, this buffer will likely not be sufficient. It is essential that you call your broker to see if you need to increase your home’s valuation, today!

Guaranteed Replacement Cost Policy

A Guaranteed Replacement Cost policy means that as long as you insured to the value your insurance company determined was required to rebuild your home at the time you bought your policy, you are fully covered even if the final rebuilding cost at claims time is much higher due to soaring material costs. However, it will be important to prepare for a potential rate increase at renewal time when the increased cost of rebuilding will likely be factored into your new premium.

The bottom line is, your home, investment properties, or commercial buildings could be significantly underinsured. It is important to have your properties’ replacement value recalculated based on the current materials, equipment and labour costs in your area. Contact your insurance broker to review your building’s valuation today. We’re here to help!