Home renovations and upgrades boomed over the last year. Some households, unable to spend their discretionary earnings on vacations and concert tickets, opted to enhance rooms, basements, and outdoor decks for entertainment and leisure. Those who were forced to work remotely constructed home offices and complex workstations. Others built spaces to enjoy their hobbies and escape the noise coming from the outside world (and a few family members).

Financing for these upgrades came from a variety of sources, including disposable household income and stimulus cheques from the federal government. Spending was further encouraged when the Feds introduced a new Canada Greener Homes Grant program which provides grants of up to $5,600 in energy-saving home upgrades. In 2020, Canadians spent more than $80 billion on home improvements, and there are few signs of this trend slowing down. Statista reports that nearly half of the surveyed Canadian homeowners plan to spend up to $10,000 on home renovations in 2021. Approximately 25% anticipate spending of up to $25,000. But with all of this investment has come a lack of oversight in one key area – homeowners insurance coverage. Are you certain that you’re covered for recent and future upgrades to your home?

Why BC Homeowners Must Review Their Insurance Policies When Making Home Improvements

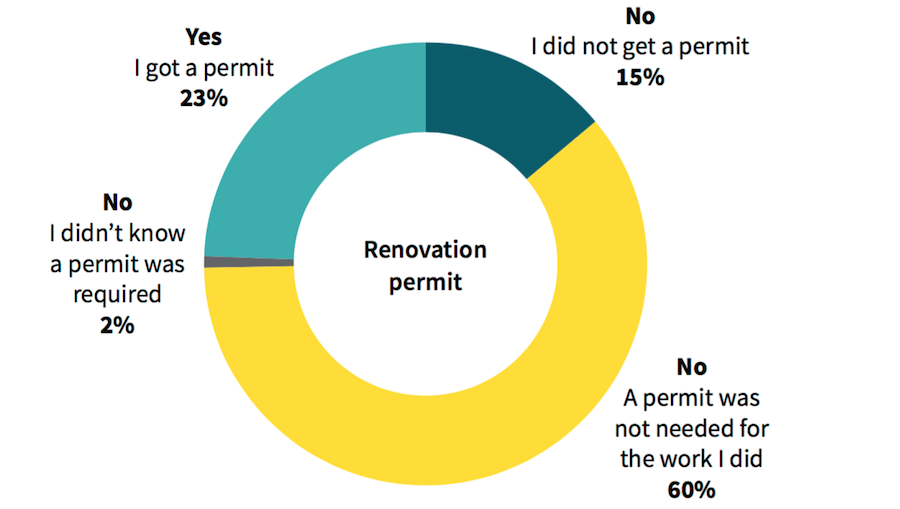

You May Need (or May Have Needed) a Permit

With residents being forced to stay at home, renovations were often accompanied by some good ol’ fashioned do-it-yourself (DIY) gumption. Data shows that only a third of those who made changes to their home hired someone to complete the work. On the surface this DIY trend is admirable, but there may be a problem. Professional home improvement experts know if/when a permit is required for an indoor or outdoor extension or retrofit. Many homeowners do not know this, and may not bother to check with their local municipality:

Source: Aviva

If a permit is required but not obtained, homeowners insurance may not cover the upgrade nor any subsequent injury and/or damage to persons and property. For example, if you add a new outdoor raised deck, invite neighbors over for a BBQ, and it collapses causing injury to guests, you could be facing financial ruin.

So, be sure to obtain all required permits and inform your insurance provider about any substantial recent and future home improvements, even if you used or plan on using a professional contractor.

A Home Improvement May Change the Value

Permanent installations and other improvements such as finishing a basement or building an addition can increase the market value of your home. This is great news as far as resale value goes, but it can also alter the home’s replacement cost/rebuild value. This should be top of mind as many homeowners face the inflated risk of seasonal wildfires or other events. A broker at Park Insurance can help you assess whether your policy is sufficient to cover the adjusted rebuild value. In fact, most insurance policies require that you report any renovations that exceed a certain value – usually $10,000. So, talking to your insurance provider is an essential step in the renovation process.

A Fundamental Difference: Home vs Home Office Upgrades

Not everyone will return to a traditional workplace environment. In fact, being forced to work from home made many professionals realize that they can stop working for someone else, and become a freelance contractor. Others have found that they can turn their hobbies into small businesses. While purchases (equipment and electronics, etc.) and permanent upgrades to add home offices may be conducive to making it all happen, these may not be covered by your home insurance if you have made the switch to running your own business. Talk to your insurance provider today about obtaining the right insurance coverage for your home-based business.

A Home Renovation May Required Specialized Coverage

Haven’t started your renovation yet? If you are planning to undertake a substantial renovation, it is essential that you contact your broker to review how your existing policy may be impacted by the renovation. For example, insurance policies often exclude coverage for water damage, vandalism, and glass breakage for buildings that are under construction. Therefore, you may need to arrange for special coverage to protect you during renovations. If you are moving out of your home during the renovation, you will also need to inform your broker as most policies will not provide coverage for homes that are vacant for more than 30 days.

We want you to be excited about your recent, present, and future home improvements. This will come with peace of mind that additions will be covered by your insurance policies. Contact Park Insurance today for a comprehensive audit and friendly conversation.